Yesterday’s session was one that basically served no purpose — none at all if you look at the fact that the indexes barely moved. Which, frankly, is a change compared to what we lived through during the first 100 days of Donald Trump. Honestly, it seems like investors are “almost happy” that nothing is happening, simply because they’re exhausted by the heavy uncertainty of recent months.

We’re like the guy falling from a 150-story building who, as he passes each floor, keeps saying: “So far, so good.” To keep it simple: as long as Trump doesn’t mess things up with some new drama, we can manage what we know

We allow ourselves to think

We can handle what we know — even if what we know isn’t much, since the promises around the talks with China are totally vague. Trump recently said he spoke with Xi Jinping, but according to official Chinese sources, Trump’s statements are complete nonsense. Then again, we all know how much trust to place in a politician who says “I’m not aware of anything” (ask Bayrou). But when a Chinese politician says “I’m not aware of anything”, it’s even worse.

That said, even though we know “officially nothing was discussed”, we all know that doesn’t mean “nothing was actually discussed.”

As my philosophical master Coluche once said:

“Those in authorized circles allow themselves to believe that a secret agreement MIGHT be made.”

And he added:

“First off, you and I are not part of those ‘authorized circles.’ Then there’s the secret agreement — which clearly means we’ll never know anything about it. And finally, there’s the conditional tense: MIGHT — so it’s not even certain!”

Even though that comedy bit is nearly 50 years old, it hasn’t aged a day. We don’t know what’s actually going on — and for all we know, the deal on tariffs between China and the U.S. might already be signed, and they’re just waiting for the right moment to announce it. That could also be the reason nobody dares to sell the market anymore. Well… we also don’t dare to buy it either, because we have no idea what’s coming in the next four days. And SURPRISE — it all starts today…

The Kind of Paralysis That Feels Good

Let me return to my guy falling from the 150th floor. I’m insisting on this because the similarities are just too perfect not to mention. You see, when you fall from a building, it’s not the fall that hurts — it’s the landing. While you’re falling, there’s no pain. You could even do stuff — like read a book. Not War and Peace — that might be a bit long — but you could get through the first chapter.

What really hurts is going from 230 kilometers per hour to a dead stop. And, yeah, the concrete hurts too. But mostly the hitting-it-at-230 part.

Well, that’s where we are: still in free fall. We’re just hoping that, by some stroke of luck, firefighters will have placed one of those giant inflatable cushions like in the movies — and that everything will be fine.

We are exactly there. Global markets have bounced back since Trump — after causing panic — started playing it cool again:

He stopped attacking Powell

He showed a softer, more diplomatic tone with China

As of yesterday, he seems more flexible on car tariffs

And we know the 90-day moratorium (a bit less now, maybe 70 days left if my math’s right) is only meant to bring countries to the negotiating table and wrap things up with a Hollywood happy ending three days before the deadline…

The markets have recovered, and everything should be fine. Except that now, we’re heading into a week from hell, and no one has the guts to take a single bet right before an avalanche of economic data and earnings reports.

So you can understand why the Dow Jones didn’t move much yesterday — up 0.28%. The S&P 500 showed even less motivation with a 0.06% gain, and the Nasdaq did worse, dropping 0.10%. In Europe, things weren’t any better: France rose 0.5%, the DAX was sluggish at +0.13%, and our good old SMI stood out from the rest of the world with a 0.72% gain.

As one “expert” said last night: “We are in a climate of cautious optimism, despite the uncertainty surrounding U.S. trade policy and its effects on the global economy.”

Yeah, I know, that doesn’t mean much — but “cautious optimism” still sounds better than “panic pessimism.” So, if we take a bit of distance from what happened yesterday — which was somewhere between almost nothing and absolutely nothing — the feeling is that the market is slowly rebuilding a sense of stability and calm, trying hard to forget that volatility can still spike 85% faster than you can say: “Lehman Brothers just went bankrupt.”

Would you like a summarized version of this for quick sharing or publication?

Let’s Not Get Carried Away

Even though the indices were in the light green zone yesterday with a level of frustration close to the maximum – and yet nobody seemed scared – I believe we shouldn’t get too carried away and must keep our heads cool. Let’s try to take stock before the avalanche of data – consumer confidence, JOLTS, GDP, PCE, employment figures – all topped off with quarterly reports from part of the Magnificent Seven, crashes down on us. Right now, it’s a bit like trying to play Jenga without shaking and without pulling out the one block that brings the whole tower down.

Here’s where we stand: the talks are dragging on and the economic bill is coming due – you can tell some Americans are starting to clench and are genuinely scared to go shopping. For now, voices like Scott Bessent’s are whispering in Trump’s ear, telling him to stay calm. The problem is, that may not last. Trump is as patient as a hungry Labrador, and it wouldn’t take much for him to crank up the pressure on Wall Street again.

Meanwhile, volatility is still doing the macarena. Even though things have improved a bit over the last few days, the bond market is all over the place, and if you were holding dollars, you might be regretting not buying your gold in Swiss francs. Scott Bessent (him again) might be bragging that the Nasdaq is “up” for the month of April, but in reality, since the tariff announcements on April 2nd, the Nasdaq is down 1.2% and still nearly 14% off its December highs.

So, everything’s fine… except for the numbers, which are often open to interpretation. Take Trump’s latest promise from less than 48 hours ago:

“We’re going to eliminate taxes for those earning under $200,000.”

Sure, Donald, sounds great. Except the tax revenues expected from that income group (under $200K) amount to $2.6 trillion, while the so-called magic tariffs only brought in $16 billion in April. You’re going to have to do a lot better than that to make up for the lost tax revenue. Even under a microscope, even magnified 10 times, those tariffs don’t cut it. And meanwhile:

– The public deficit keeps exploding,

– Treasuries are tumbling,

– And the dollar has dropped 7% since January.

In short: investors are fleeing America like a cockroach-infested pizzeria. Even if some believe there’s a method to Trump’s madness, most prefer to exit now and maybe come back later. We’ll have to see what this week’s data avalanche brings – maybe it paints an unexpected picture that lets the Fed pull off a cliffhanger during next week’s meeting. Just the thought of Powell staying hawkish and refusing to cut rates is enough to make the markets tremble… Imagine Trump dusting off Powell’s termination letter and forwarding it to HR.

Everything’s Fine on the S&P500, But…

This morning, looking at the indices, it feels like all is well and we’ve found some semblance of calm. I’m sure you think so too. Yet if we dig deeper into the mindset of middle America, we have to wonder how long we can keep going in this crappy atmosphere before becoming “Great Again.” Trump came back to save the economy, but 100 days in, everyone’s panicking.

Consumers see the economy as a cliff we’re about to step off. The tariffs have wrecked confidence – morale is knocked out cold. Even if we’re still hoping for a miracle tonight with the consumer confidence data, it’s hard to say everything’s fine! 53% of Americans say their finances are getting worse — a record not seen since the pandemic. Everyone’s tightening their belts, and plans for houses, cars, or vacations are going out the window. No visibility, fears of empty shelves like 2020… The average American is clamping down. End of story. For now. Even the housing market is coughing, with loans struggling to get repaid.

And worse: as families cut spending, companies are starting to panic too. American Airlines, Chipotle, Domino’s… they’re all cancelling forecasts because they just can’t see what’s ahead – visibility is zero, uncertainty at maximum. It’s like flying a plane around Everest in thick fog with your altitude gauge broken — you don’t know if you’re above 29,000 feet or below. Consumption is slowing, shelves are thinning, hiring plans are going into deep freeze. Even among Republicans, the mood is less euphoric. Sure, they still back Trump, but even they are starting to feel the sting. America is quietly sliding into a psychological recession. On paper, things still look okay – growth, jobs, and all that. This week’s numbers should confirm it. If all goes well. Let’s not forget: American growth is always said to be driven by the consumer. If the consumer bails on us, it’s game over.

Polls Are Scary (But That’s Their Job)

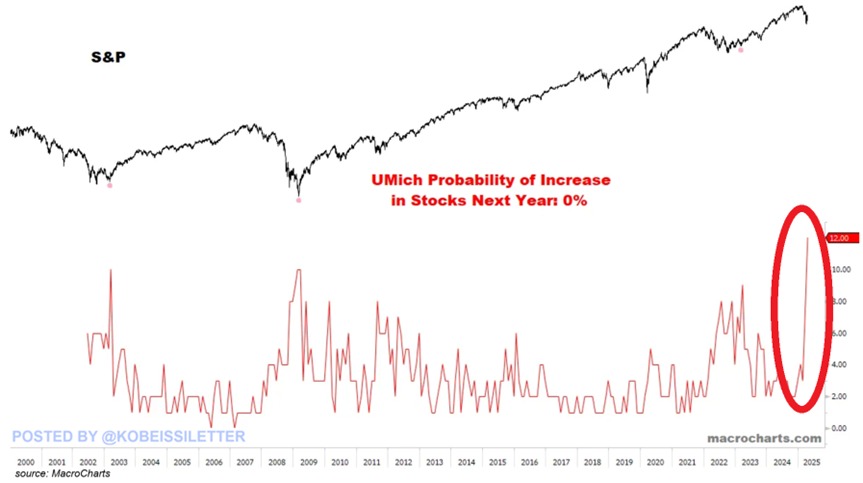

By the way, even though markets are holding up and are at 10-day highs, American consumers’ pessimism about the stock market is at record levels… According to a University of Michigan poll, 12% of Americans believe there is zero chance the market will rise in the next 12 months. That’s triple the number from two months ago – and worse than the lowest points of 2009, 2020, and 2022. Meanwhile, 44.5% of respondents think the market will actually fall within the year.

Would you like a shorter summary version of this translation for a newsletter or headline briefing?

In short, the mood is festive… And that’s where it gets funny – that’s where we realize that sometimes, we actually enjoy scaring ourselves. Just now, I painted an absolutely crappy picture of the average American’s psychological state – and I topped it off with a pretty lousy survey. And maybe that’s actually the only good news of the day. Yes, because before jumping to apocalyptic conclusions, let’s keep a few things in mind:

This “national survey” is based on a whopping 500 to 600 households.

500–600 households, out of 350 million people in the United States… Let’s just say, in terms of representativeness and diversity, we’ve seen better.

And most of the respondents are from the Michigan area.

So yes, it’s a snapshot.

Yes, it sets a tone.

But claiming this is “American opinion” as a whole is a bit of a stretch. And not just a stretch – it’s completely off. “It’s like asking penguins their opinion on air conditioning in Dubai.” It’s a psychological signal, interesting for the overall mood, but certainly not a comprehensive study to bet your house on. That said, I actually think it’s a fantastic contrarian signal. Yep – I’m trying to stay optimistic. All this to say that yesterday, the market didn’t do much, but it’s definitely thinking a lot, and those holding its fate right now are: consumer confidence, JOLTS, GDP, PCE, employment figures, Apple, Microsoft, Amazon, and Meta.

So now what???

This morning, Japan is closed, China is doing nothing – they’re probably on the phone with Trump – and Hong Kong is up 0.5%. Oil is at $61.57, gold is at $3,321, and Bitcoin is at $94,400. On the news front, HSBC – Europe’s biggest bank – posted better-than-expected results, thanks to strong wealth management performance and the solidity of its investment bank. HSBC also announced a share buyback of up to $3 billion.

As for Trump, we’re circling back once again on the car topic:

After announcing a 25% tariff on foreign cars, the President pulled off one of his signature backpedals.

Point 1: No double penalty: automakers won’t have to pay both car tariffs and steel/aluminum tariffs.

Point 2: Automakers can even get a partial refund on taxes they’ve already paid.

Point 3: Trump wants to give factories time to bring production lines back to the U.S.

Ford and GM are smiling publicly, but rebuilding factories will take years. Morgan Stanley estimates the tariff would have raised the average car price by $6,000 (+10 to 12%). Trump is backing off a bit to avoid tanking prices and choking the industry ahead of his triumphant visit to Detroit. In short: Trump is easing off slightly, but the logistical nightmare remains very real.

Nvidia under pressure

For two weeks now, Nvidia’s been under pressure – since being banned from selling its H20 chips in China. Huawei took the opportunity to launch its own AI chip, the Ascend 910D. On paper, it’s progressing fast… but in reality, it’s less powerful and more power-hungry. Huawei might hold its ground in China, but internationally, it’s dead on arrival: too expensive, too political. The real risk for Nvidia is if China forces local companies to drop some of Nvidia’s products. Technically, Nvidia is still way ahead, but the economic war is on. For now, markets are panicking more than necessary – and according to experts, Nvidia is hit, but not sunk.

As for today’s numbers, we’ll have plenty to digest: consumer climate in Germany, then U.S. consumer confidence and the JOLTS report. Consumer Confidence is expected at 87.7 and JOLTS at 7.49 million job openings. On the corporate side, we’ll hear from SOFI, UPS, Coca-Cola, Pfizer, Spotify, Altria, Visa, Starbucks, Snap, Novartis, Deutsche Bank, Porsche, and Logitech…

At the moment, futures are up 0.12%, and we’re waiting to see if we hit the pavement or not.

So subscribe to Soleyam s channel and facebook, have a great day, and I’ll see you tomorrow to find out if the American consumer is about to crack – or not!!!

See you tomorrow!