I have to admit that ever since I started working in this field, I’ve always been amazed at how we can go from laughter to tears in a matter of minutes. Normally, that’s something you’d say about an actor—but here, we’re talking about an entire market.

Last night, I came across a sentence that made me want to roll on the floor laughing. A sentence so absurd, it proves we have the IQ of a spoiled mussel and that yes, we are capable of going from laughter to tears in under 12 minutes. The sentence is:

“The S&P 500 closes higher. Investors begin to look past the conflict between Israel and Iran.”

It’s M-A-G-N-I-F-I-C-E-N-T.

You have to admit it’s quite something to see that just four days after hostilities began, stock markets have already sized up the conflict and switched into “don’t care” mode. Oil is back around $70 or so, defense stocks are getting smashed, and oil companies are under pressure because ALL THE EXPERTS SAY: Iran won’t close the Strait of Hormuz, so oil at $80, or $120—or even $150—is clearly overhyped.

And on top of that—fabulous news—Iran already seems ready to negotiate. At least, that’s what the Wall Street Journal claimed yesterday, which was immediately confirmed by Trump. The President thinks the Iranians should have thought of that sooner, but still left the G7 to try to broker a peace deal between the two sides. His spokesperson, Emmanuel Macron, announced it to the press yesterday…

We already talked about this a few days ago: every armed conflict brings its initial wave of panic, but it always ends in a bull market. Still, to think we’d bounce back so quickly—when the Iranian military is threatening a fiery apocalypse via tweets on X—felt far-fetched. Yet here we are: Wall Street and other global markets ALREADY got their smile back and resumed their upward march.

After briefly freaking out over Israeli strikes on Iran, the markets basically said:

“Well, maybe it won’t turn into World War III just yet.”

The result: the Dow Jones rose 317 points, the S&P 500 climbed 0.9%, and the Nasdaq jumped 1.5%. In Europe, the DAX rose 0.78%, France gained 0.75%, and Switzerland was down 0.45%—because apparently we no longer need a safe haven now that war is no longer interesting.

But careful, the mood is still tense: people were already nervous before the war due to tariffs, so if oil takes off again, inflation could still be a serious issue in the coming weeks.

The Fed meets today for two days. They’re not expected to touch interest rates, but all eyes will be on Powell’s press conference Wednesday. Because right now, one wrong word… and it’s total panic again.

The war isn’t over, though

Still, as I said at the beginning of this piece, the market has already priced in the Iran-Israel war and moved on. What happens next in the real conflict is still a big question mark, but for now—as long as it doesn’t get worse than what we already know—there’s no reason to panic.

That said, I’d like to point something out: yesterday, the Iranian military promised to launch so many missiles on Tel Aviv that it would be unlike anything ever seen in history. And, by the way, you could even watch the bombing live yesterday on The Sun’s website.

We’ve reached the point where live bombing streams are being broadcast. If anyone was wondering whether humanity could sink lower in its mediocrity and depravity—I think we have our answer.

So, Iran wants to negotiate, Trump wants to get involved, and in the meantime Israel is bombing Iran’s national TV station, and Iran claims to have shot down 4 F-35s—which Israel says is fake news.

Anyway, I’m no expert, but this doesn’t exactly look like a ceasefire within 48 hours followed by embassy reopenings next week.

But since markets have decided they no longer care, let’s move on. Because THE FINANCIAL AND ECONOMIC EVENT OF THE WEEK is clearly the Fed kicking off its two-day meeting in just a few hours.

So let’s talk about the Fed and Jerome “Too Late” Powell.

The FED

The Fed has been in “wait and see” mode for a while now, and we all know it. But why is the Fed just observing and not doing anything? Well, because out there, it’s a real mess — and if I had to choose between smashing both my knees with a hammer or taking Powell’s job, I’d say: “WHERE THE HELL IS THAT HAMMER?!”

Between a trade war that never really ended and an actual war in the Middle East (even if we stopped caring for the past 24 hours and investors are starting to look beyond the Israel-Iran conflict — as someone once said), the U.S. economy is limping along. Growth is slowing, companies are pulling back on hiring, and consumers are hesitant to pull out their credit cards. Cards that are already maxed out at rates that would make the Corleone family jealous.

You can imagine that Powell’s job isn’t easy, even though it basically boils down to: “Do I cut now or later?” — with a side note: “What if I have to raise rates again to re-cool inflation?”

The equation is relatively complex, full of unknowns, and one certainty: if nothing changes, Trump could very well launch Operation RISING LION — not on Tehran, but on the Fed and Powell himself. So the Fed is expected to keep rates unchanged tomorrow night, while keeping a close eye on inflation, which will likely dominate headlines in the coming weeks.

For now, inflation is holding steady around 2–2.5%, but if it starts climbing again — say goodbye to the rate cuts Wall Street is hoping for. In short, the fog is thick… and everyone is scrutinizing the Fed’s forecasts like Powell has the power to change the world. One thing’s for sure: this well-timed conflict isn’t making Powell’s job any easier. Even if Wall Street has moved past the military tensions, Powell still has to factor them into his decisions.

And in Asia, They’ve Moved On Too

This Tuesday morning, the Bank of Japan did… exactly what everyone expected: nothing. Rates remain at 0.5%, no surprises. However, they did announce a gradual slowdown of their government bond purchases, aiming to gently exit their ultra-loose monetary policy and give long-term rates some breathing room.

Timing is delicate: Japan’s economy is sluggish (GDP contracted in Q1), inflation remains stubborn (3.5% in April — above the target for three years now), and rice prices are surging due to a shortage. In short, a perfect storm for major BOJ headaches. The Nikkei and Topix responded to the non-decision with a small uptick, but overall, Asian markets stayed cautious. Understandably so: the Iran-Israel conflict casts a heavy shadow, especially after Trump’s call to evacuate Tehran. Even if the White House walked it back, nerves are raw.

Add to that a week packed with central bank meetings (Fed, SNB, BoE, PBoC…), and you get the perfect cocktail for markets stuck in a “lukewarm” state. Especially since U.S. futures dropped again during the Asian session, cooling down yesterday’s relative enthusiasm. In China, indices fell by 0.3%, despite a 5% growth forecast for H1. In Singapore, exports are plunging. In Sydney, markets are dragging. Only South Korea’s KOSPI is showing some optimism thanks to tech and a hint of political stability.

In summary: no one wants to make a big move before the Fed speaks tomorrow, the BOJ is stalling, markets are geopolitically tense, and traders are watching the news like they’re expecting to get all the answers to invest risk-free and make easy money. Gold is at $3,407, oil is around $70.70, Bitcoin is at $107,500, and the 10-year yield sits at 4.44%.

News and Reflection

Elsewhere in the news, AMD jumped 9% yesterday, riding the wave of excitement over its new AI chips — Instinct MI350 — and its Helios system. After a lukewarm reception last week, investors seem to have had a change of heart over the weekend. The relative calm in the Middle East allowed markets to refocus on fundamentals, and AMD took full advantage. Nvidia can’t supply everyone, and AMD might snag some market share, especially from Amazon Web Services, according to several finance experts who can actually talk about something other than the economy.

Even if the MI355 is still a notch below Nvidia, the MI450, expected within a year, could really shake things up. In the meantime, AMD’s stock is on fire… and Wall Street is beginning to believe — cautiously.

And then the big news in France yesterday was a corporate transfer that made waves: Renault’s CEO, Luca de Meo, is leaving to join Kering and try to save Gucci. Not sure if he can make Gucci cool again like he did with the Renault 5 and Alpine, but the fact remains: Renault lost 9%, while Kering gained 12%! That has to feel pretty good — being “transferred” and pulling off that kind of score. Even the best hedge funds wouldn’t have dared dream of such a “pair trade.”

On the Bond Side

And finally, the U.S. managed to offload $13 billion in 20-year debt at a 4.942% yield. Apparently, that’s “good news”: investors showed up, the government didn’t have to add extra incentives, and experts agreed that “everything is fine, no buyer’s strike.”

But behind the polite smiles of the Treasury, the reality is… a little more tense. Because this week is America’s debt Grand Slam. The government plans to borrow:

$58 billion in 3-year notes on Tuesday,

$39 billion in 10-year notes on Wednesday,

$22 billion in 30-year bonds on Thursday.

And this is where it gets real. At 30 years, we’re talking serious risk and zero visibility for whoever signs that check. Few buyers, long duration, and a Trump who blows hot and cold with his trade war rhetoric — it doesn’t exactly scream “trust us with your money.” Especially considering the latest figures:

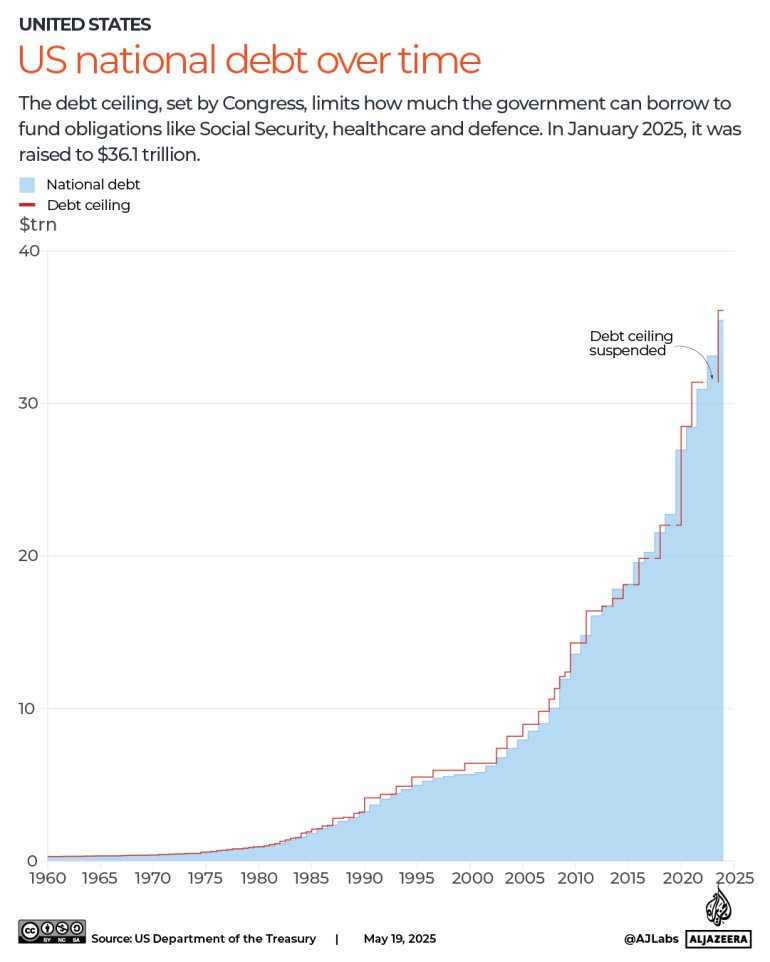

25% of all federal revenue now goes just to pay interest on the public debt of $37 trillion.

Per year:

Total U.S. government revenue ≈ $5 trillion

Interest payments ≈ $1.2 trillion

Total expenditures ≈ $7 trillion

A quick glance at the math and you’re left thinking: this can only end well… Not today, not tomorrow, but one day, we’re going to hit that wall.

As one expert put it yesterday:

“Yes, there will always be buyers… but they’re going to start demanding one hell of a premium to keep financing America’s future.”

In other words: they’ll lend — but it won’t come cheap.

And meanwhile, rates are climbing, other countries are making their debt more attractive, and the US economy is showing signs of fatigue.

We might be slowly sliding into structural distrust — not a crisis yet… but you can hear a faint squeaking in the background.

So yes, that 20-year auction went well. But it may just have been a brief reprieve… before the real questions start hitting as early as Tuesday.

Because the world still wants to believe in America — but believing comes at a cost.

Today’s Numbers

After the BOJ’s conference, focus will shift to the ZEW index in Germany and Europe.

In the US, we’ll be watching Retail Sales, Industrial Production, and Business Inventories.

Later in the day, we’ll also get an increasingly influential figure: the Atlanta Fed GDPNow — that real-time-ish estimate of economic growth. It’ll probably tell us a few things.

For now, the war is “over” — at least on Wall Street — and the world’s great powers, a.k.a. the G7, have once again released one of those press statements they’re so good at — just to prove, once more, how utterly useless they are:

In a heartbreakingly original communiqué, the G7 reminds us that Israel has the right to defend itself, that Iran is evil, and, above all, that Iran must never get the bomb.

They also demand, in a last-minute flash of wisdom, a ceasefire in Gaza and a resolution to the ‘Iran crisis’ — as if this was some mind-bending puzzle and THEY had finally figured out the solution in under 24 hours — something we mere mortals never thought of because we’re obviously too dumb.

Honestly, we could recycle their statements year after year and no one would notice.

This morning, futures are going all over the place in sync with announcements and tweets from various players.

When I woke up at 4 a.m., they were down 0.5% — now they’re almost flat.

So yeah, while bombs are falling, the G7 throws words, Powell meditates, Trump tweets, inflation lurks in the shadows, and the world keeps spinning in circles.

Have a great day everyone — and see you Thursday, because tomorrow is Swissquote Trading Day and I’ll be hosting it as the Master of Ceremonies, so I can’t be everywhere at once.

See you Thursday then…